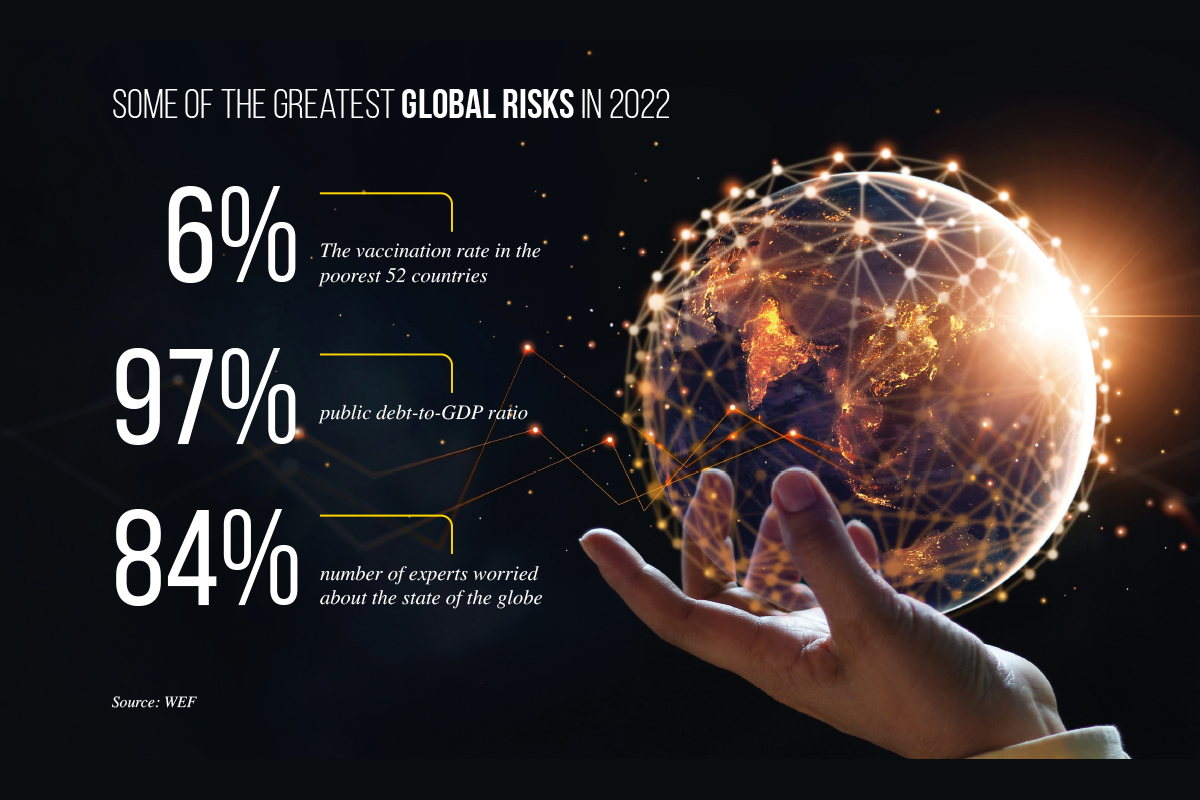

With the world roiled by socioeconomic and political turbulence, we ascertain the state of the global economy statistically

We’ve all seen the headlines every day. They’re unmissable, screaming at you from the paper or television.

- “Inflation at its highest level since 1970s”.

- “Central banks raise rates again”.

- “Ukraine-Russia war heads into its ninth month”.

- “Commodity prices soar to all-time highs”.

- “Semiconductor shortage impacts industry”.

And on, and on.

At a bare minimum, inflation has severely dented consumer and industry sentiments, with a wide-ranging impact on the global economy. All of this has been brought by something resembling a perfect storm; two years or so ago, if someone told you a global pandemic would be followed by energy shortages, soaring inflation, and a war brought about by geopolitical tensions, it would have sounded like something out of a very active imagination. And yet, here we are.

This unique systemic shocks are reshaping the global landscape as we know it, and we paint a picture of how the very structure of the world order is being reshaped through the below charts.

Inflationary Pressures

In many countries, inflation is on a runaway spree, as much as double or more of projections from December 2021, as per OECD data. Lithuania is an example of how badly hit some parts of the world economy are, with inflation at 15.5% as of June 2022 versus a projection of closer to 3%. Among major economies, the UK is closer to 9% versus a projection of 4.5%, while the USA is holding its own, even if its June 2022 figure of close to 7% exceeds its December 2021 projection of close to 5%. Asia is not as impacted; Indian inflation is at approx. 7% versus projections of 5%, much like the USA, while China seems to have inflation under control.

An Increase in Lending Rates

By way of response to inflationary pressures, central banks across the world have tightened their monetary policy and raised lending rates. While most have not matched the rate of inflation to temper economic shocks, it will likely curb demand and inflation to a degree.

Home truths

According to Knight Frank Research, house prices across 56 countries and territories increased by 10.3% on average in 2021. Turkey had the highest annual price growth rate of 59.6% in the year to Q4 2021, followed by New Zealand and the Czech Republic at 22.6% and 22.1% respectively. India demonstrated a price increase of 2.1%, and only three markets saw prices decline – Malaysia, Malta, and Morocco.

Rising Commodity Prices

Conventional logic dictates that commodity prices are a good hedge in flationary times as it is a leading indicator of inflation, highlighting economic changes before the economy as a whole awakens to it. It is equally true that commodity prices soar on the back of demand, and the graphs below reveal this too. As the pandemic deflated the global economy, commodity prices cooled off, before once again taking off as consumer demand was on the rise. Geopolitical shocks (such as the Russian invasion of Ukraine) served to send this higher still, in particular fertiilisers, as the natural gas needed to make it was in short supply.

A Food Crisis in the Offing?

Another fallout of Ukraine’s invasion has been a food shortage, as it is the granary of Europe and a major supplier of food grains to the world. This, coupled with a rise in fertiliser prices, is causing the prices of food to spiral. Prices are considerably higher than before, although it dropped 23.8 points (14.9%) from its peak in March this year to 135.9 points in October 2022 as per the FAO Food Price Index. However, it remained 2.7 points (2%) above its value in the corresponding month last year.

A Gloomy Growth Outlook

And so, as inflation rears its head, prices of food, commodities, and houses soar, economic growth too gets impacted. For instance, Gross Domestic Product (GDP) in the G20 area fell 0.4% quarter-on-quarter in the second quarter of 2022 after rising 0.5% in the first quarter, according to provisional estimates. This can largely be attributed to a contraction in China, where GDP fell by 2.6% quarter-on-quarter after rising by 1.4% in Q1 2022. A similar contraction was witnessed in India (1.4%), South Africa (0.7%), and the United Kingdom and United States of America (0.1% in both countries) as well. The Indian slowdown can be attributed to decreases in government spending and net trade (exports minus imports). With oil in high demand, projections for Saudi Arabia’s real GDP growth is now about 2.2% higher in Q2 2022.