In the sweltering heat of Mumbai, the most dangerous number on a data center CFO’s dashboard isn’t the bottomline, it’s the wet-bulb temperature

Words by Karan Karayi

From the air-conditioned silence of a control room in Navi Mumbai, the summer of 2026 looks less like a season, and more akin to a surcharge.

Outside, the asphalt is melting as the thermometer climbs into the high 30’s. Inside, the facility manager is fighting a losing battle against thermodynamics. As the ambient temperature climbs, the massive chillers on the roof scream louder, sucking in megawatts of power just to keep the server racks at a benign 22°C. On the monitor, the Power Usage Effectiveness (PUE) ratio (the holy grail of data center efficiency) creeps upward from a respectable 1.4 to a ruinous 1.7.

For the Chief Financial Officer sitting at the headquarters of this Global Capability Centre (GCC), this tick upward is not an engineering glitch, but an inflation spike. For decades, the “India Advantage” was predicated on a simple arbitrage: labor was cheap, land was available, and power, while erratic, was manageable. But as the mercury breaches 40°C with punishing regularity across the Indo-Gangetic plain, a new economic reality has set in. The heat is no longer just a weather event, but a tax that becomes increasingly heavy to bear.

Welcome to the era of “Cooling Inflation”, where the cost of fighting the sun is threatening to erode the operational margins of India’s digital backbone.

The Meteorological Tax

To understand the crisis, one must look at the physics of the “Heat Tax.” A data center is effectively a massive heater (the servers) wrapped in a massive refrigerator (the cooling system). In temperate climates like Stockholm or Dublin, operators can simply open the windows (a technique known as “free air cooling”) for much of the year. In India, where the air itself is a blast furnace for four months annually, that is not an option.

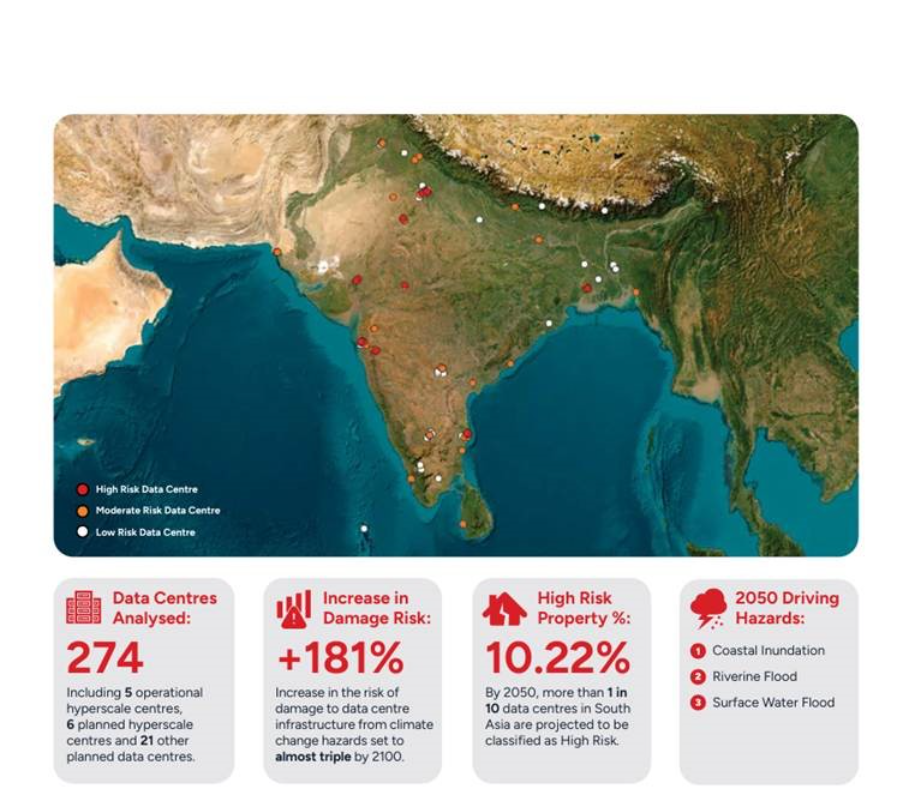

According to the 2025 XDI Global Data Centre Risk Report, the geography of the cloud is colliding with the geography of climate change. The report explicitly flags Uttar Pradesh and Tamil Nadu (home to the booming Noida and Chennai operational hubs respectively) as being among the “Global Top 25” riskiest data center regions by 2050.

But one need not wait for 2050. The financial pain is already here.

Data from ST Telemedia Global Data Centres (STT GDC) India suggests that cooling alone accounts for roughly 40% of total energy consumption in Indian facilities. When ambient temperatures rise, the efficiency of air-cooled chillers plummets. To maintain uptime, operators must run backup compressors and consume water at voracious rates.

Market projections for 2026 indicate that for legacy facilities relying on air cooling, this “thermal penalty” is driving operational costs up by an estimated 15-20% during peak summer months. For a CFO budgeting for a flat operational expenditure, the summer surplus is a nasty surprise. The “PUE of 1.4” promised in the brochure is a winter statistic; the summer reality is a PUE of 1.7, and the difference is paid in hard cash to the power grid.

The Stranded Asset Trap

The crisis is starkest for the “middle-aged” facilities built between 2015 and 2020. Designed for an era of standard cloud computing (5-8kW per rack), these buildings rely on raised floors and perimeter cooling. Think of giant air conditioners blowing cold air under the floorboards.

Enter the AI boom. The new NVIDIA Blackwell chips and high-density AI clusters run at 40kW to 100kW per rack. They run hot; hot enough to melt the innards of a standard server if airflow is interrupted for seconds. To cool these beasts with air is like trying to put out a forest fire with a garden hose.

This creates a “Stranded Asset” risk. As Cushman & Wakefield’s H1 2025 India Data Centre Update notes, vacancy rates in some operational clusters have crept up not because of a lack of demand, but because of a mismatch in quality. Tenants want liquid-ready, high-density halls. Landlords are holding leases on air-cooled buildings that are chemically incapable of hosting the next generation of tenants without a massive capital injection.

The choice for these operators is brutal: spend millions in CAPEX to retrofit operational buildings with Direct-to-Chip liquid cooling loops (which creates a logistical nightmare involving plumbing over live servers) or watch their assets turn into digital warehouses for low-value “cold storage” data.

The Water Credit Risk

If power is the immediate cost, water is the existential credit risk. In the desperate bid to keep temperatures down, evaporative cooling towers are the weapon of choice. They are effective, but they are thirsty.

A widely cited study from Cornell University estimates that global AI demand could withdraw between 4.2 and 6.6 billion cubic meters of water annually by 2027. In a water-stressed nation like India, this is a liability that trascends the nature of a mere environmental statistic.

Banks and ESG-conscious investors are beginning to view “Water Intensity” (liters consumed per kilowatt-hour) with the same suspicion they view carbon. A facility in Chennai that guzzles millions of liters of municipal water during a drought is a regulatory target. We are seeing the first signs of “Water Neutrality” becoming a covenant in loan agreements. If a data center cannot prove it is water-positive (i.e., recycling more than it consumes) the cost of capital rises.

This forces a second, expensive pivot: “Zero-Water Cooling.” Technologies that use closed-loop systems are available, but they come at a premium. The CFO is thus caught in a pincer movement: the heat demands more water, but the regulators demand less. It’s a slippery slope that’s hard to escape.

The “Edge” Mirage

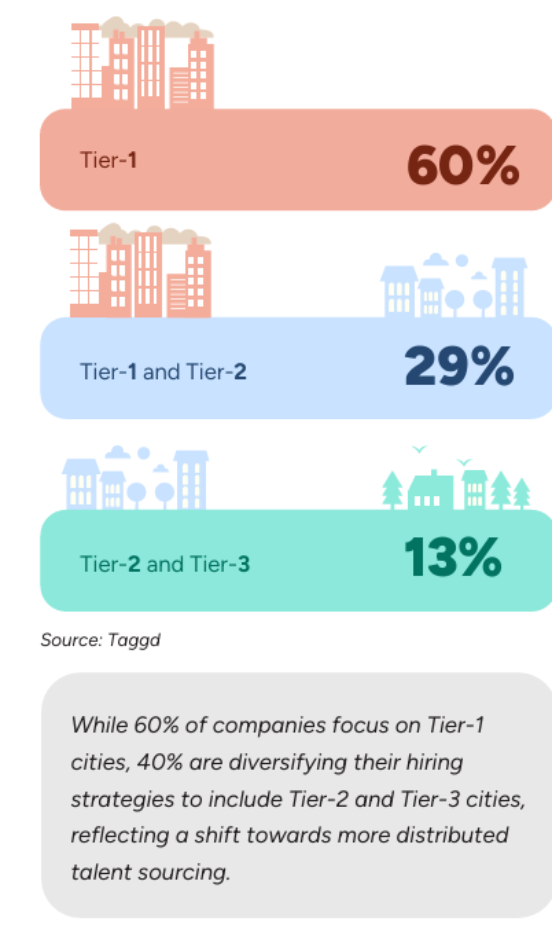

The optimistic counter-narrative is the “Edge”, or the idea that data centers will move away from the sweltering, concrete jungles of Mumbai and Delhi to cooler, cheaper Tier-2 cities. Indeed, reports like the Taggd GCC Report 2025 highlight that 40% of new setups are eyeing cities like Bhubaneswar or Coimbatore.

But physics is stubborn. While land is cheaper in the hinterland, the infrastructure is thinner. In Tier-2 hubs, the grid reliability gap often forces operators to run on diesel generators for longer periods. As you might imagine, this is an expensive and dirty habit that negates any PUE savings. Furthermore, data has gravity. The “latency” required for financial trading or real-time AI inference anchors these facilities to the submarine cable landing stations in Mumbai and Chennai. They cannot move. They must sweat it out.

The Cold Hard Truth

As the Indian summer approaches, the boardroom conversation is shifting. The metric of success is no longer just uptime, you could argue it’s thermal resilience.

The cooling inflation crisis is forcing a bifurcation in the market. On one side are the new, shiny AI fortresses, which are liquid-cooled, water-neutral, and priced at a premium. On the other are the legacy air-cooled sheds, struggling to keep their PUE down as the thermometer goes up, effectively paying a “Heat Tax” on every transaction.

For the Indian data center industry, the warning from the thermometer is clear: Innovate, liquid-cool, or prepare to burn cash. The 45°C future is not a forecast, but an invoice awaiting payment, one way or another.